Exercise 1

Jai Broome

21 November, 2016

require(ggplot2)

require(dplyr)

require(knitr)1 Simple Octave/MATLAB function

I’ll skip over this since I figure anyone wanting to follow along is already familiar with R

1.1 Submitting Solutions

You won’t be able to submit this for credit, but hopefully you still find this useful

2 Linear regression with one variable

Here I read in the data, split it into X and y, and generate starting values for theta

q1data <- read.table("data/ex1data1.txt",

sep = ",",

col.names = c("population", "profit"))

q1data$ones <- 1

q1data <- q1data %>% select(ones, population, profit)

X <- select(q1data, -profit)

y <- q1data$profit

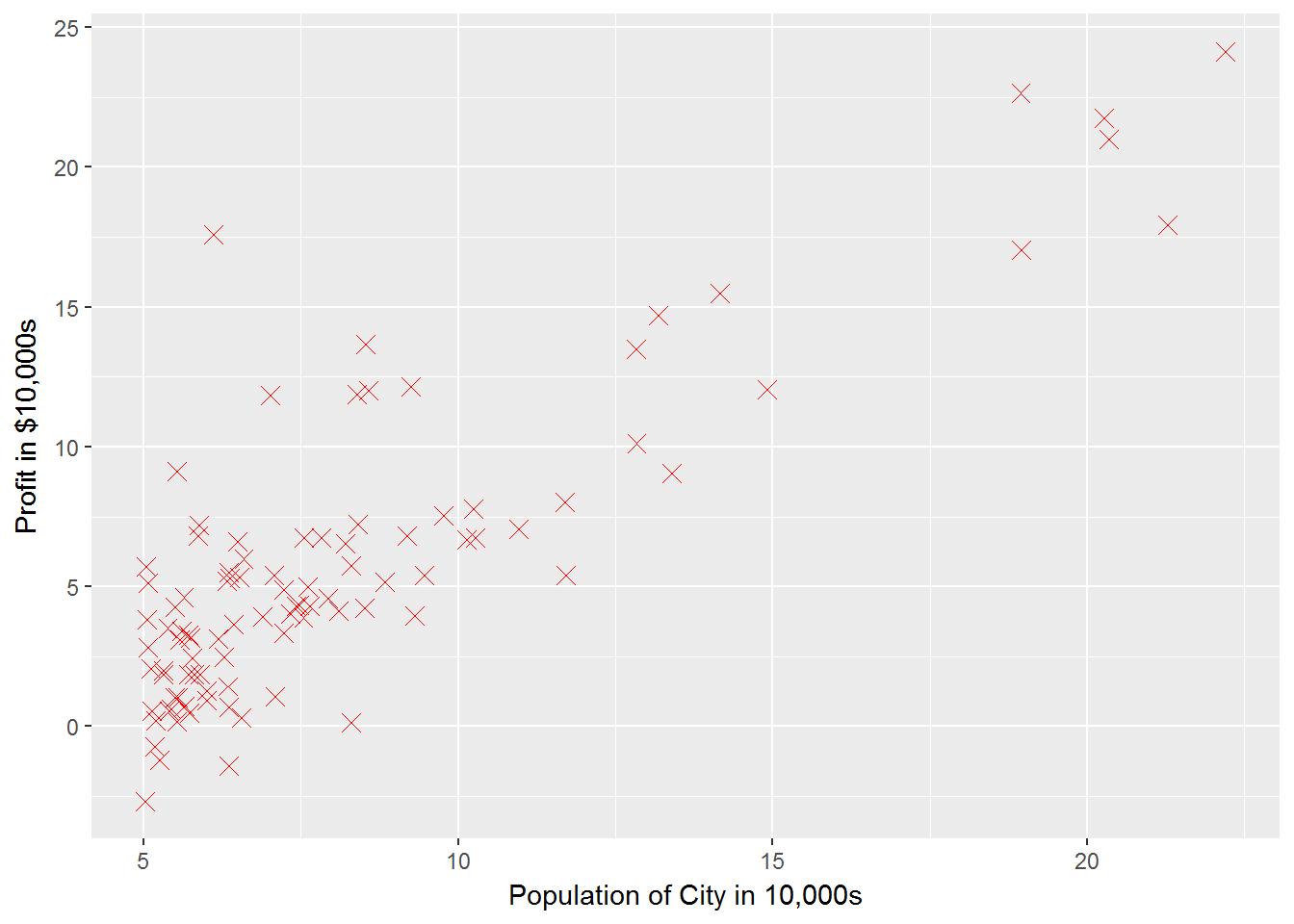

theta <- rep(0, times = 2)2.1 Plotting the Data

g1 <- ggplot(q1data, aes(x = population, y = profit)) +

geom_point(shape = 4, color = "red", size = 3) +

xlab("Population of City in 10,000s") +

ylab("Profit in $10,000s")

g1

2.2 Gradient Descent

iterations <- 1500

alpha <- 0.01Functions are defined in a separate script so they can be accessed for other assignments. See ?knitr::read_chunk

read_chunk("ex1/ex1_chunks.R")computeCost <- function(X, y, theta, lambda = 0){

if(is.null(dim(X))){

X <- t(data.frame(X))

}

m <- nrow(X)

pred <- theta %*% t(X)

sqError <- (pred - y) ^ 2

cost <- (1 / (2 * m)) * sum(sqError)

reg <- (lambda / (2 * m)) * sum(theta[-1]^2)

J <- cost + reg

gradient <- (1 / m) * sum((pred - y) * X[, 1]) # first element unregularized

for(j in 2:length(theta)){

gradient <- c(gradient, ((1 / m) * sum((pred - y) * X[, j]) + lambda * theta[j] / m))

}

return(list(J=J, gradient=gradient))

}gradStep <- function(thetaj, alpha, gradj){

thetaj - alpha * gradj

}Note that in the loop, thetas get stored in a temporary variable for simultaneous updating.

gradientDescent <- function(X, y, theta, alpha, iterations, lambda = 0){

if(length(theta) != ncol(X)){stop("theta and X are nonconformable")}

J_history <- data.frame()

for (iteration in 1:iterations){

a <- computeCost(X = X, y = y, theta = theta, lambda = lambda)

J <- a$J

gradient <- a$gradient

J_history <- rbind(J_history, c(J, iteration - 1, theta))

thetaTemp <- vector()

for(j in 1:length(theta)){

thetaTemp <- c(thetaTemp, gradStep(theta[j], alpha, gradient[j]))

}

theta <- thetaTemp

}

# for final iteration

J <- computeCost(X = X, y = y, theta = theta, lambda = lambda)$J

J_history <- rbind(J_history, c(J, iteration, theta))

thetanames <- rep("theta", times = length(theta) - 1)

for(i in length(thetanames)){thetanames[i] <- paste("theta", i, sep = "")}

colnames(J_history) <- c("loss", "iterations", "theta0", thetanames)

return(J_history)

}computeCost(X, y, theta)## $J

## [1] 32.07273

##

## $gradient

## [1] -5.839135 -65.328850Should be 32.07

2.3 Debugging

Pay particular attention to indexing in these exercizes, because unlike Matlab, R does start indexing at 1

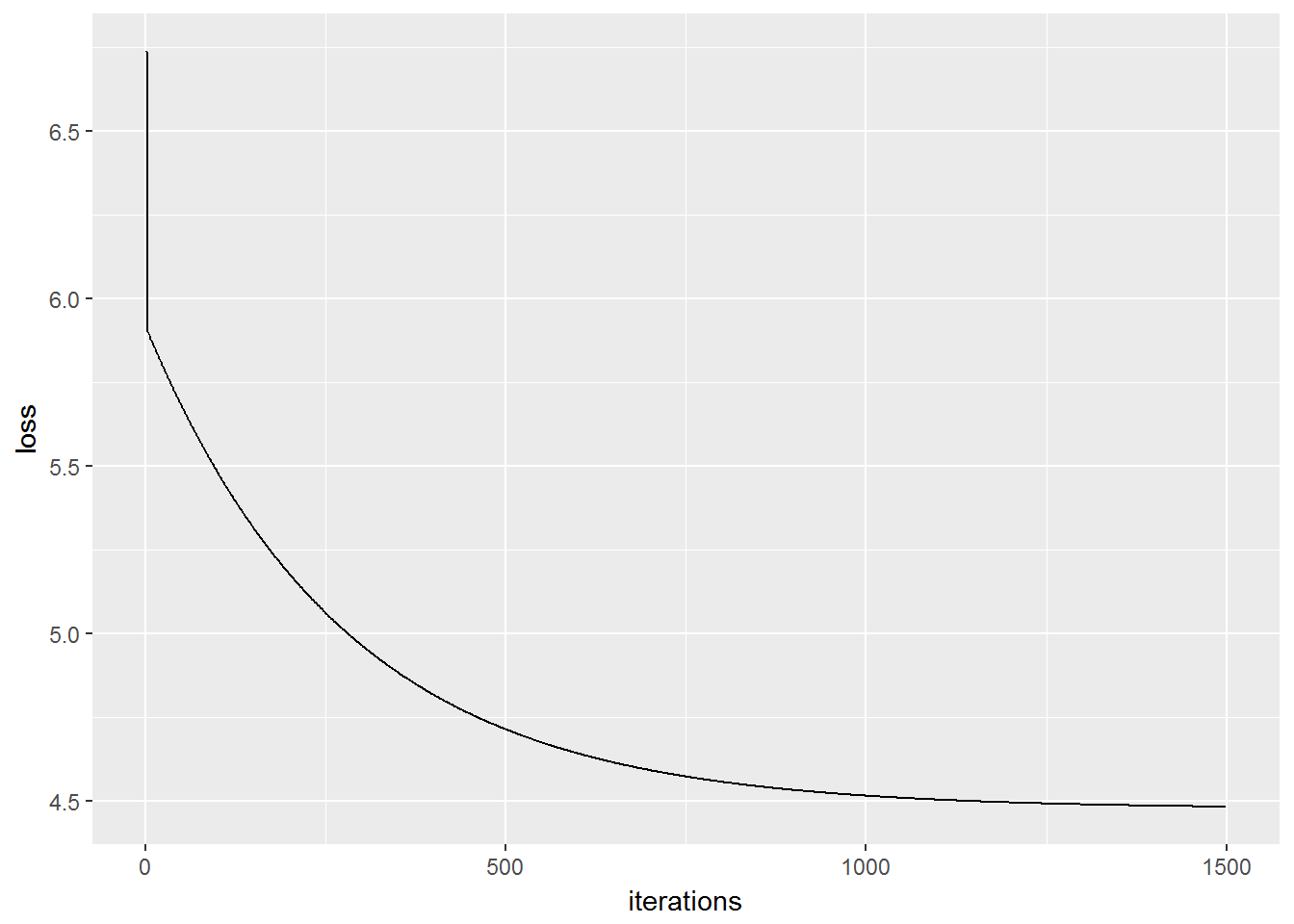

jhist <- gradientDescent(X, y, theta, alpha, iterations)

jhist <- jhist[2:(nrow(jhist) - 1),] #makes graph more interpretible ggplot(jhist, aes(x = iterations, y = loss)) + geom_line()

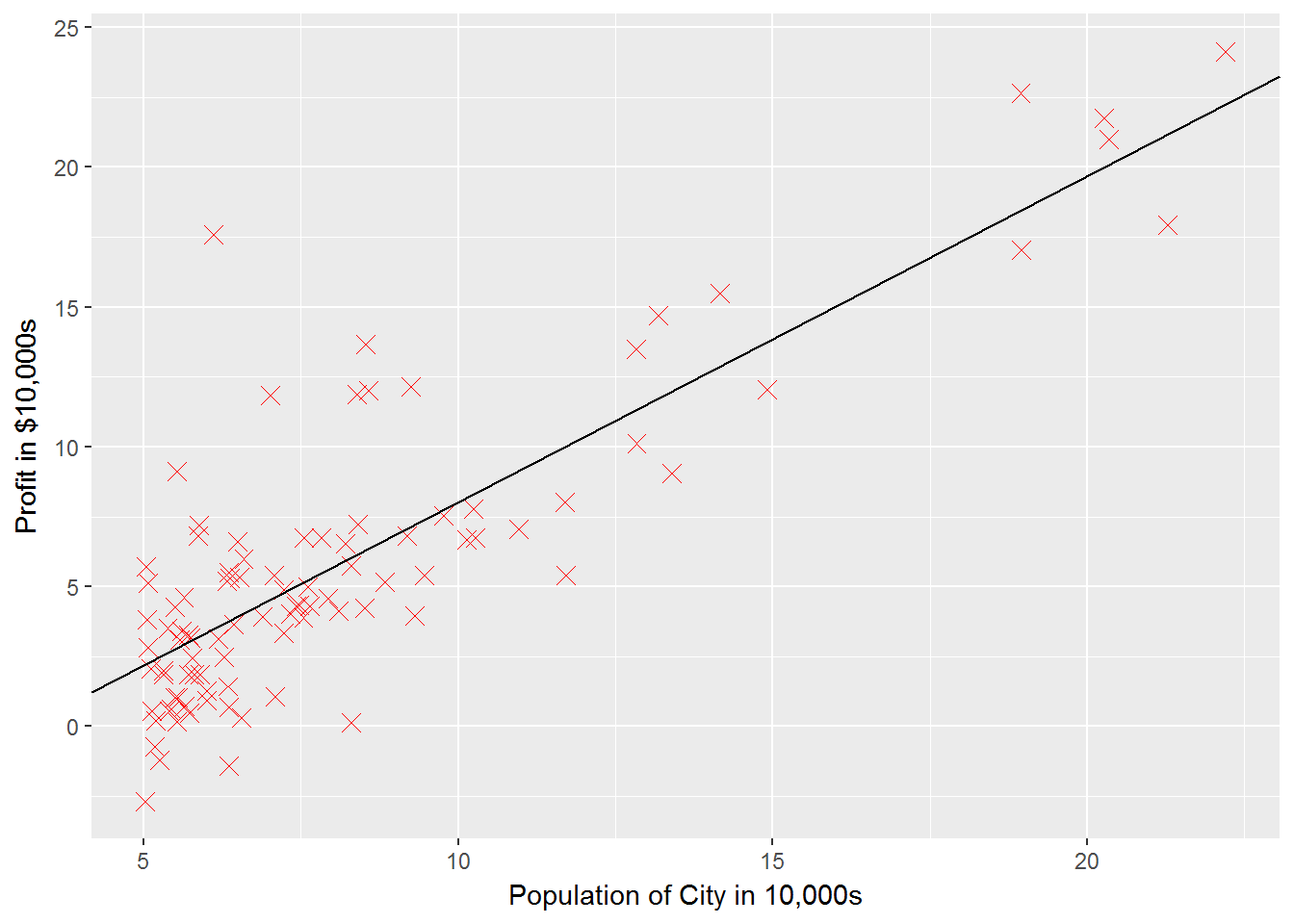

g1 + geom_abline(slope = tail(jhist$theta1, n = 1), intercept = tail(jhist$theta0, n = 1))

2.4 Visualizing \(J(\theta)\)

I skipped over this section since the code is already written in Matlab by the course instructors. See the assignment page for the images that show how different values of the thetas yield different costs

3 Optional exercises

These are still incomplete. I’m planning on returning to these after making it through the main course content